Chapter 8 : The Standard Cost Accounting System Part 2: Journal Entries, Cost Variances, And Reports

Learning Objectives

After studying this chapter, you should be able to:

1. Discuss the role of a standard cost accounting system (SCAS) in responsibility accounting.

2. Explain the meaning of a cost variance, and calculate and interpret the variable costs' spending variances.

3. Calculate and interpret the variable costs' usage variances.

4. Calculate and interpret the fixed overhead variances.

5. Prepare the journal entries for an SCAS, and the cost variance report.

6. Design a high-quality SCAS with management reports useful for operational control and performance evaluation.

6. Prepare a list of attributes needed in a relational database to prepare Standard Cost reports in an REA environment.

Introduction

Chapters 4, 5, and 6 presented actual and normal JOCASs and PCASs. These cost accounting systems are mainly based on actual costs. By themselves, however, actual costs are not particularly useful to management in controlling daily operations and evaluating performance. For these decision-making needs, actual costs should be compared against standard costs.

The standard costs, prices, and quantities and the standard manufacturing cost equation reside in the SCAS LAN database. This information is accessed by the production LAN's MRP II system as needed in shop floor operational planning and control. The SCAS also includes a report generator that, in world-class enterprises, can provide real-time cost variance information as well as summary reports. In this way, the SCAS can provide high-quality information for its cost management objective.

In addition, standard costs can be used in the SCAS journal entries to represent the product's cost in WIP, FGI, and COGS. Some enterprises use standard costs and cost variances strictly as planning, controlling, and evaluating techniques. Cost variance information is available within the JOCAS or PCAS LAN, but actual costs are used in the journal entries. An example of a JOCAS that reported cost variances was discussed in Chapter 5 (see Exhibit 5-22). Other companies enter standard costs in the general ledger accounts and journalize cost variances.

As explained in the last chapter, when actual costs and standard costs differ, the difference is a cost variance. A cost variance can be either favorable or unfavorable. A favorable cost variance results when actual costs are less than standard costs. An unfavorable cost variance occurs when actual costs are greater than standard costs. Although variances are excellent devices for gauging economic and operating performance, management accountants must take care to ensure that they are used properly and do not cause counterproductive behavior.

Cost Variance Reporting, Responsibility Accounting, And Motivation

LEARNING OBJECTIVE 1

Discuss the role of a standard cost accounting system (SCAS) in responsibility accounting.

A standard cost developed jointly by management and employees responsible for the costs can be a motivating influence for employees and result in higher productivity. Generally, people are more motivated to do a good job if they clearly understand what is expected of them and believe they will be rewarded for their efforts.

Using cost variances as fault-finding devices and placing too much reliance on them in evaluations may, however, motivate people to engage in counterproductive acts such as delayed maintenance, bickering over cost allocations, or even falsifying data. Indeed, most people's needs are too diverse and changeable to be satisfied by a single evaluation criterion, such as a cost variance. Rewards for learning additional skills, reducing spoilage, increasing equipment uptime, and suggesting successful improvements, to name just a few, are part of the evaluation-reward-motivation systems of many world-class enterprises.

Cost management, through control of shop floor activities, is an important component in a firm's success and profitability. In assigning responsibility to the individuals in a position to exercise control over those costs, shop floor employees become cost-conscious as they become aware of results. The cost-consciousness tends to reduce costs and encourage improvement in performance in all activities of the organization.

The SCAS, however, should not be used as an excuse to conduct “witch hunts.” The focus should be on supporting the production process by helping workers solve problems and achieve the standards they participated in setting. Spending too much time investigating previous period cost variances and blaming people can often bring about results contrary to those intended.

Ideal And Practical Standards

In describing the SCAS's role as a responsibility accounting system, it is important first to consider how the standards are set. Because standards are goals that are used to judge actual performance, a key question is, “Just how demanding should standards be?” Should they assume theoretical perfection, or should they assume various factors that prevent perfect performance? Standards can be based on ideal or practical operating conditions. For example, a small unfavorable variance implies very good performance if ideal standards are set, while the same variance implies average performance, at best, if practical standards are used. A small unfavorable variance from an ideal standard may not lead to further investigation, whereas the same variance based on practical standards may lead to investigation and corrective action.

Ideal standards are set as goals toward which employees work for continuous improvement, a concept of world-class manufacturing. Variances from these standards will probably always be unfavorable, but continuous improvement will result in the variances becoming smaller over time. Thus, the SCAS, when using ideal standards, will have to output trend analysis reports, often in graphic form. By showing the reduction in cost variances over time (i.e., movement toward the ideal standards), these reports can provide long-range, continuous improvement information.

Practical standards are tight but achievable. They do not tolerate abnormal waste and lost time, although they allow for normal machine downtime, employee rest periods, and the like. Both favorable and unfavorable variances result from the use of these standards. Generally, they have been considered to be most useful in determining how effectively and efficiently present operations are being carried out.

These standards can be met or surpassed by actual performance, but only if high efficiency is achieved. They are indeed within the achievable range of most employees, yet difficult enough that employees feel as though they have accomplished something of value when the standards are attained. Employees are motivated by practical standards, especially if they've had input into their development, and will normally put forth their best efforts to achieve them.

If management is trying to compete against world-class enterprises, however, cost variances from practical standards may not provide the kind of performance information the firm needs. Enterprises using standards that typically ignore continuous improvement and have avoidable inefficiencies built in will not be able to compete against world-class enterprises that are continually striving to eliminate waste and inefficiencies of all kinds.

The best standard for today's competitive environment is one that seeks to improve future performance. Long-run continuous improvement is measured by the movement toward ideal standards. When ideal standards are used to calculate cost variances, the reduction in cost variances over time signals this improvement. An enterprise that uses practical standards also needs long-range graphical trend analysis of the change in standards. The difference between ideal and practical standards is the long-run continuous improvement goal. Thus, this difference should be decreasing over time.

Managing By Exception

The use of standard costs makes possible the concept of management-by-exception. In traditional and world-class, manufacturing and nonmanufacturing, profit and nonprofit enterprises, the most important scarce resource is time.

Computers are used for managing by exception and tracking cost variances.

This is especially true in JITs that need to respond quickly to changing custom needs and production problems that can lead to jidoka (defined in Chapter 2). Thus, shop floor personnel must be able to distinguish between variances that can be ignored and those that should be investigated. To make this distinction, managers set upper and lower limits of acceptable variances from standard. So long as cost variances remain within the limits set, no special attention is needed. When an unfavorable cost variance falls outside the limits, the people responsible are expected to determine its cause. Whenever possible, immediate corrective action is taken to eliminate the cause and bring operations back in line with standard.

If the variance is favorable, management can reward superb performance and learn why this favorable variance occurred. A favorable variance, however, is not always indicative of good performance. It may mean that an error was made in setting the standard or that another type of problem exists. For example, purchasing inferior quality materials for a price less than standard can create a favorable cost variance. Using less materials than the standard quantity also results in a favorable variance. However, both of these events may be real problems! Therefore whether a variance is unfavorable or favorable, it should be investigated if it falls outside the limits.

Even if a variance never exceeds the limits, managers may still want a variance report when variances consistently come close to the Limits. A variance that is close to the limits period after period may indicate that the standard is inappropriate or that the performance regarding that standard needs an occasional check by management.

Even very large variances may be out of management's control, however. Utility, payroll tax, and insurance rates are typical examples. Such variance-causing items may be included on the variance report for information purposes, but do not necessarily require follow-up by management beyond adjusting the standard prices.

Further, managers may view some variances as more significant than others depending on what they measure. Certain items, such as usage of direct materials in some operations, may be deemed so critical that any deviation from standard should be reported and investigated. Also, in certain operations, any variance should always be investigated whether it falls outside the limits or not. For example, anything dealing with equipment maintenance warrants careful scrutiny. Preventive maintenance keeps equipment fine-tuned to run more efficiently. Equipment that is not properly maintained uses more oil and fuel (or electricity) to run and can entail major costs when it breaks down.

Reporting Variances

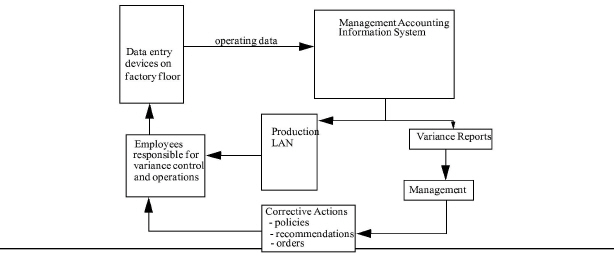

The key objective of variance analysis and reporting is to isolate off-standard performance quickly and correct it. The operational control loop is illustrated in Exhibit 8-1

|

. Steps necessary to install this operational control loop include the following:

Step 1. Set the standards, prepare the standard cost card, and develop the budgeted manufacturing cost equation. This step was covered in Chapter 7.

Step 2. Collect operating data and measure actual performance. With the use of computers, automated production equipment, and online data collection and entry devices, measurement may be real-time, whereas in manual-based systems, measurement may be monthly.

Step 3. Process operating data and calculate variances.

Step 4. Report variances to the managers and workers who are responsible for them and have authority to take corrective action. The key for corrective action and operational control is the timely arrival of variance information and immediate action by managers and operating personnel. Variances occur as operations are performed. Therefore, the quicker the variances are reported, the sooner corrective action can be taken, if warranted. For example, if an operation is using excessive amounts of direct materials and the variance indicating this abnormal usage is not reported until a month after the fact, management may not know about the problem and therefore can take no corrective action during that month. Cost control must be applied at the place and time where the cost variance originates.

Step 5. Determine the significance of each variance. Some variances require investigation, others do not. In turn, investigation may or may not reveal the need for corrective action.

Step 6. Take appropriate corrective actions. Setting new policies, making recommendations, and giving specific orders to supervisors and workers involved directly in operations are all forms of corrective action. Because no set rules or parameters may exist about when to investigate or take corrective action, managers and workers often must use their own judgment. A fundamental characteristic of world-class manufacturing is that control (i.e., investigation, problem identification, and corrective action) occurs on the shop floor as operations are performed. The role of the SCAS as a responsibility accounting system is to capture data on the sources and causes of cost variances and indicate whether corrective actions have been taken. In its daily operational control role, the SCAS reinforces the need for control at the source by requiring input on control activities.

Step 7. Change performance, if possible, to bring actual performance in line with standard performance. Supervisors and workers can change tasks and activities to prevent future variances from occurring from the same causes.

Step 8. Revise standards if those previously set are no longer relevant. Standard costs must be revised when prices, rates, operations, product or service specifications, or other circumstances change to such an extent that the existing standards no longer represent a good measure of performance.

Reducing Record-keeping Costs

Information-processing efficiency is increased when record-keeping costs are reduced. Materials requisitions and labor time tickets can be prepared in advance of production using the production LAN's bill of materials, MRP and/ or MRP II programs, and the standard quantities from the standard cost cards.

|

INSIGHTS &, APPLICATIONS Nulife's Variance Analysis |

Nulife purchases large volumes of a special compound from a pharmaceutical company that it mixes with water to produce a health drink called Tigerade. The standard costs for direct materials, direct labor, and overhead to produce one case of Tigerade are presented in Exhibit 8-2. This exhibit also includes the manufacturing cost equation and actual production and cost data for July. |

In an actual CAS, when a perpetual inventory system is used, the accountant must continuously recalculate changing actual unit costs. In a periodic inventory system, RMI costs may be calculated by assuming some inventory flow pattern (FIFO, LIFO, moving average, and so on). In an SCAS, costs can be assigned to WIP, FGI, and COGS accounts based on standard prices and quantities for each cost element. Rather than valuing completed output by performing the cost allocations required in process costing, an SCAS will use the standard absorptive manufacturing cost (SAMC).

|

Exhibit 8-2 The Standard Cost Card for Nulife's Tigerade Sports Drink |

||||

|

Standard Cost Card for One Case of Tigerade |

|

|||

|

Items |

Standard Price |

Standard Quantity |

Standard Cost |

|

|

|

Direct Materials |

$ 1.00/lb |

3 lb./case |

$3.00/case |

|

|

Direct Labour |

$10.00/DLhr |

2 DLhr/case |

$ 20.00/case |

|

Variable Overhead |

$1.50/DLhr |

2 DLhr/case |

$ 3.00/case |

|

|

|

Fixed Overhead [based on a quota of 10,000 cases per month] |

$ .60/DLhr |

2 DLhr/case |

$ 1.20/case |

|

Standard Absorptive Manufacturing Cost [SAMC] |

|

|

$ 27.20/case |

|

|

|

|

|

|

|

|

Monthly Tigerade manufacturing costs = $12,000/month + $ 26.00/case |

||||

|

Actual Production Data and Costs for July |

||

|

Items |

Actual Costs |

Actual Quantities |

|

Direct materials |

$1.10/1b. |

40,000 lb. purchased 30,000 lb. requisitioned |

|

Direct labor |

$9.50/DLhr |

17,500 DLhr worked |

|

Variable overhead |

$25,000 |

|

|

Fixed overhead |

$12,100 |

|

|

Actual output |

|

9,000 cases of Tigerade |

For example, if the SAMC in the printing department of a textbook publisher is $5 per book and the pages for 1,000 books were printed last month, then the journal entry amount transferring printed pages from this department to the binding department would be $5,000 (see Exhibit 6-4 and journal entry 8 in the PCAS). For a JOCAS, if the SAMC for a one-pound box of chocolate-covered cherries is $6.50 and 100 boxes are produced in job 247, then the job's cost is $650.00 for journal entries 8 and 9 (see Exhibit 5-1 and the COGM and COGS journal entries).

Obviously, some of the clerical time and record-keeping costs saved through such simplification is offset by time spent in deriving standards, keeping them current, and calculating and reporting cost variances. The real cost savings occur in the long run, during the implementation of the SCAS when inefficiencies may be identified and corrected and waste uncovered, and later when variances are reported, investigated, and corrected.

Scas Cost Variance Formulas

LEARNING OBJECTIVE 2

Explain the meaning of a cost variance, and calculate and interpret the variable costs' spending variances.

Generically speaking, there are only two types of cost Variances: spending (price) variances and efficiency (usage) variances.In this section, the spending variances for the variable manufacturing costs (direct materials, direct labor, and variable overhead) will be illustrated first. Next, the usage variances will be calculated for the variable manufacturing costs, followed by the spending and usage variances for fixed overhead. Finally, alternative methods for calculating overhead variances will be considered. The Nulife Sports Drink Company will be used to illustrate these calculations:

Spending Variances For Variable Costs

The basic formula for a variable cost spending variance is:

Variable cost spending variance = Actual quantity purchased x (Standard price - Actual price)

= AQp x (SP - AP)

DIRECT MATERIALS PRICE VARIANCE. The direct materials standard price is usually based on either the expected price during the period the standard is in effect or on the price existing at the time the standard is set. Normally, this group decision-making activity involves the purchasing department aided by the management accountant.

Many factors influence the price paid for materials, such as quantities purchased, delivery method used, quantity discounts, and rush orders. Serious study should be given to handling and storage procedures to determine whether they are the most efficient possible. Such analysis should indicate the most economical quantities to purchase, the best delivery method at the lowest cost, and the most economical ways of storing and handling in-plant materials.

The direct materials price variance measures the difference between what is paid for a given quantity of materials and what should have been paid according to the standard price that has been set. The formula used to compute this variance is:

Direct materials price variance = AQp x (SP - AP)

In July, Nulife incurred the following price variance for Tigerade's direct materials:

Direct materials price variance

|

|

= 40,000 pounds purchased x ($1.00/lb. / $1.10/lb.) |

|

|

= <$4,000> unfavorable |

Explaining the price variance calculation is relatively simple. Forty thousand pounds were purchased at an average price that is $0.10 per pound higher than the standard price. Ten cents per pound multiplied by the 40,000 pounds purchased results in a cost overrun of $4,000-in other words, an unfavorable spending variance of $4,000.1 While explaining the calculation to shop floor personnel is relatively easy, identifying the cause of the variance may be more difficult.

Generally, the purchasing agent has control over the prices paid for materials and, therefore, is responsible for purchase price variances. This is the first person who should be consulted in attempting to identify the cause of the variance. In Nulife's case, the unfavorable price variance resulted from the pharmaceutical company unexpectedly raising its price $0.10 per pound. The purchasing agent has negotiated a price of $1.05 per pound for the next six months. The new direct materials standard price will be $1.05 per pound next period. In a high-quality SCAS, the explanation for any price variance is recorded on the purchase order. This information is then available as soon as it is known for input into the SCAS database and for use by the MRP II LAN and the marketing LAN in updating sales prices (if possible).

Caution must be exercised to make sure that the purchasing agent is not buying poor-quality material, at a lower cost, to realize a favorable price variance. The poor-quality material will cause problems later in production. Also, the purchasing agent may increase the purchase order quantity to obtain a lower unit cost. Large inventories, however, require large automated stockrooms and sophisticated inventory tracking systems, which drive up nonvalue-added costs. Maintaining these systems generates even more nonvalue-added activities and costs. Thus, if this purchasing price variance is the only performance evaluation criterion for the purchasing agent, he or she may be motivated into these dysfunctional decisions.

In some instances, however, someone other than the purchasing agent may be responsible for a direct materials price variance. The production manager, for example, may schedule production in such a way as to require overnight delivery of materials, thus driving up the price paid for them. The following are several additional reasons why actual direct materials prices may differ from standard direct materials prices:

• Change of vendor

• Change of lot size

• Change in price by vendor

• Change in specifications

• Change in the marketplace

Two considerations relevant to the design of a high-quality SCAS become obvious. First, the SCAS needs to capture data on the cause of the variance when it first becomes known. Second, once the cause has been identified, its source has to be input into the SCAS so that responsibility can be properly assigned for performance evaluation. If the source and cause of cost variances are not captured within the SCAS, then it cannot provide accurate and relevant information for operational control and performance evaluation. In that case, the SCAS may not lead to proper evaluation and rewards and, therefore, may not promote the desired motivations and goal-congruent behaviors for daily control activities.

DIRECT LABOR RATE VARIANCE. The development of a standard direct labor cost requires identifying the direct labor classification needed for the operation and the wage rate paid for that labor skill. Rates for labor are often determined by union negotiations or by the prevailing rate in the area where the company is located. The key objective is to match the operations with the labor classifications called for.

The direct labor rate variance measures any deviation from standard in the average hourly rate paid to employees plus the average hourly payroll taxes and fringe benefits paid for them. The formula used to compute this variance for July's production of Tigerade at Nulife is:

Direct labor rate variance

= Actual DLhr worked x (Standard rate - Actual rate)

= AQp x (SP - AP)

= 17,500 DLhr worked x ($10.00/DLhr - $9.50/DLhr)

= $8,750 favorable

The same basic formula is used for both the direct materials and the direct labor spending variances. The difference between the standard price (rate) and the actual price (rate) is multiplied by the quantity purchased. For direct labor, the hours purchased always equal the hours worked because labor is actually “purchased” (paid for) after it is used. Similarly, with a JIT purchasing system, the quantity of materials used and purchased is equal.

As with the direct materials price variance, this variance's calculation is relatively simple to explain. The average labor rate (including the direct labor wage rate plus employer payroll taxes and fringe benefits) was 50 cents per hour less than budgeted. For the 17,500 DLhr actually worked (i.e., for the actual quantity purchased), this resulted in a cost savings of $8,750.

In many companies, the rate paid workers is set by union contract. Therefore, in such instances, rate variances tend to be small. The way workers are used can lead to rate variances, however. Skilled employees with high hourly rates of pay can be assigned tasks that require little skill and call for low hourly rates of pay. Such misuse of workers will result in unfavorable direct labor rate variances because the actual hourly rate of pay will exceed the standard rate authorized for the particular task being performed. Also, poor scheduling of work may cause unfavorable rate variances. In addition, workers may have been paid excess rates during peak seasonal periods in order to obtain the necessary work force.

In the Nulife example, just the opposite situation happened during July. The favorable rate variance resulted from hiring part-time help. Total actual labor cost was $166,250. These temporary workers earned a lower hourly wage rate and cost Nulife less in payroll taxes and fringe benefits than the company would have spent if it had used regular workers and paid them overtime. The result was an average savings of 50 cents per hour when the total direct labor costs were averaged over the total hours worked.

VARIABLE OVERHEAD SPENDING VARIANCE. The variable overhead spending variance is the amount budgeted for the number of direct labor hours worked minus the actual VOH costs incurred. This variance is usually the responsibility of the person or persons in charge of such VOH cost items as indirect labor, utilities, maintenance, supplies, and so forth. These costs should be in line with the amount of work performed. For the Nulife case, the VOH spending variance is:

|

Budgeted costs based on actual hours worked (17,500 DLhr x $1.50/DLhr) |

$26,250 |

|

Less actual variable overhead costs |

<25,000> |

|

Variable overhead spending variance |

$ 1,250 favorable |

While this “formula” may look different from the formula used for direct materials and labor, it is really the same, just in an unfactored form. To illustrate this, the “actual VOH price” is $1.43 per DLhr (rounded). A price per DLhr must be calculated to compare against the standard price (VOH POR), which is also per DLhr. The quantity used in the formula must then he DLhr as well. Using the basic formula:

VOH spending variance = AQp x (SP - AP)

= 17,500 DLhr worth of VOH items purchased x ($1.501DLhr - $1.43/DLhr)

= $1,225 favorable

The $25.00 difference between these two versions of the formula is due to a rounding error in using the $1.43 average price per DLhr worked. The actual average VOH price per DLhr is $1.42857. Thus, using the unfactored format originally presented avoids this rounding error. The unfactored format can be used for all three variable cost spending variances.2 In many SCASs, only the total actual VOH costs may be recorded, not the individual actual prices and rates. In these situations, the unfactored format may be simpler and more accurate. With the implementation of an ICBIS, though, fields within computer database records usually exist for storing the unit prices. Also, calculation of unit prices and rates may make the information more usable for the shop floor, where people think in terms of per pound and per hour prices.

The favorable VOH spending variance for Tigerade could have been caused by cost decreases in variable overhead items or the efficient use of these items, or both. To better understand why this is true, consider how the VOH line in the standard cost card is calculated. While total VOH is budgeted by using a DLhr basis, VOH items are not really purchased by the labor hour. Lubricating oil may be purchased in 50-gallon drums; drill bits and saw blades by the box of one dozen; and nails, tacks, brackets, and the like in 25-pound boxes. To apply all the VOH items to individual products, they are averaged over the activity basis that causes their use (i.e., direct labor hours for Tigerade). Since the VOH applied is computed by using a standard price (VOH POR) based on direct labor hours, the average actual VOH costs are also averaged over the actual direct labor hours worked to calculate an average VOH price per DLhr for the variance comparison.

Thus, the average actual VOH price per DLhr worked results from the prices of the VOH items purchased and the amount used for the hours actually worked. If the price for certain VOH items is less than budgeted and/or the amount used is less than budgeted for a DLhr, then this variance will be favorable. The variance itself, however, does not provide insight into which factors caused it.

The management accountant should break down the VOH spending variance into the elements comprising it. Exhibit 8-3

|

Exhibit 8-3 Detailed Analysis of the Variable Overhead Spending Variance for Nulife Corporation |

|||

|

Detailed Comparison of Flexible Variable Overhead Budget Costs with Actual Variable Overhead Costs For the Month Ended July 31 |

|||

|

Variable Overhead Elements |

Flexible Budget for 17,500 DLhr Actually Worked |

Less: Actual VOH Costs |

VOH Spending Variance |

|

Indirect labor (17,500 DLhr x $0.70) |

$12,250 |

$13,250 |

<$1,000> U |

|

Utilities (17,500 DLhr x $0.25) |

4,375 |

2,400 |

1,975 F |

|

Maintenance (17,500 DLhr x $0.55) |

9,625 |

9,350 |

275 F |

|

Total (17,500 DLhr x $1.50) |

$26,250 |

$25,000 |

$1,250 F |

|

Explanation of variances: Indirect labor variance of $1,000 U is caused by a raise in pay. Utilities variance of $1,975 F is due to an earlier policy to conserve energy. Maintenance variance of $275 F is caused by a new expert maintenance system. |

|||

illustrates how the variance is presented as a line-by-line analysis. This more complete analysis is much more useful to managers who are responsible for different elements. Although the total VOH spending variance may be small and favorable, such a report is usually necessary. For example, a small favorable VOH spending variance may be the result of large individual favorable and unfavorable overhead item variances offsetting one another.

The second column in Exhibit 8-3 is titled “Flexible Budget for 17,500 DLhr Actually Worked.” A flexible budget is a budget amount calculated using the actual hours worked. It is an “after-the-fact” budget prepared by using the cost equation and the hours actually worked. This is necessary because variable costs exist. Variable costs change in total with changes in production volume and the number of hours worked.

For example, in preparing the original budget for Tigerade, the production quota was 10,000 cases. Using the standard quantity for direct labor (2 DLhr per case), 20,000 DLhr were originally budgeted to be worked, and $30,000 of VOH was budgeted in total (VOH POR of $1.50 per DLhr multiplied by 20,000 DLhr budgeted). The original budgeted $30,000 cannot be compared to the $25,000 actually spent, though, because this amount was spent in working only 17,500 direct labor hours. Of course, if fewer hours are worked, less total VOH should be spent.

For a valid comparison, the budget has to be adjusted to what it should he for the DLhr actually worked. For 17,500 DLhr, only $26,250 in VOH should have been spent (VOH POR of $1.50 per DLhr multiplied by 17,500 actual DLhr worked). This is the “flexible” budget amount that should be compared against the actual VOH costs incurred for the same 17,500 DLhr worked. The spending variance formula automatically adjusts for this by comparing (AQp x SP) to actual cost. This can be seen in the unfactored format of the variance formula.

Usage Variances For Variable Costs

As with the variable costs spending variances, there is one basic formula for the variable costs' efficiency variances:

Variable cost usage variance

|

|

= Standard price x (Standard quantity allowed - Actual quantity used) |

|

|

= SP x (SQA - AQu) |

The standard quantity allowed (SQA) is the total amount of an input item that should have been used for the actual production volume. The formula for SQA is:

SQA = Standard quantity x Actual output

For example, if one case of Tigerade (in Exhibit 8-2) is made, then:

• SQA Direct materials = 3 lb. per case x 1 case = 3 lb.

• SQA Direct Labour = 2 DLhr per case x 1 case = 2 DLhr

• SQAVOH = 2 DLhr per case x 1 case = 2 DLhr

If ten cases of Tigerade are made, then:

• SQA Direct materials = 3 lb. per case x 10 cases = 30 lb.

• SQA Direct labour = 2 DLhr per case x 10 cases = 20 DLhr

• SQAVOH = 2 DLhr per case x 10 cases = 20 DLhr

If 9,000 cases of Tigerade (the actual output) are made, then:

• SQA Direct materials = 3 lb. per case x 9,000 = 27,000 lb.

• SQA Direct Labour = 2 DLhr per case x 9,000 = 18,000 DLhr

• SQA VOH = 2 DLhr per case x 9,000 = 18,000 DLhr

The more cases of Tigerade produced, the more direct materials, direct labor, and VOH items will be used. These are variable costs. The SQA calculation is a flexible budget adjustment for quantities.

In July, 9,000 cases of Tigerade were produced. There were no beginning or ending WIP inventories, or output loss. If partial effort exists in beginning or ending WIP, or in output loss, the partial effort needs to be accounted for by computing equivalent units of production (EUP) for each cost element. This is a standard PCAS. To illustrate, assume an ending WIP inventory in July of 200 cases, 100 percent complete with respect to direct materials, 50 percent complete for direct labor, and 25 percent complete for VOH. The EUPs for July are:

EUP for direct materials = 9,000 completed cases + (100% x 200 cases)

= 9,200 EUP

EUP for direct labor = 9,000 completed cases + (50% x 200 cases)

= 9,100 EUP

EUP for VOH = 9,000 completed cases + (25% x 200 cases)

= 9,050 EUP

Then:

SQADirect materials = 3 pounds per case x 9,200 EUP = 27,600 pounds

SQA Direct labour = 2 DLhr per case x 9,100 EUP = 18,200 DLhr

SQAvoh = 2 DLhr per case x 9,050 EUP = 18,100 DLhr

Throughout the remainder of this chapter, we will continue to ignore the existence of partial effort in beginning WIP, ending WIP, and/or output loss (spoilage). This is to emphasize the concepts and calculations involved in an SCAS. In reality, though, it is important to remember the need for EUP calculations in process system SCASs.

DIRECT MATERIALS USAGE VARIANCE. The direct materials usage variance measures the difference between the actual quantity of materials used in production and the quantity that should have been used (SQA). The formula used to compute this variance is:

Direct materials usage variance = SP x (SQA - AQu)

For the Tigerade example:

Direct materials usage variance = $1.00/lb. x (27,000 lb. - 30,000 lb.)

= <$3,000> unfavorable

Like the spending variances, this usage variance is fairly easy to explain. For the 9,000 cases of Tigerade that were produced in July, only 27,000 pounds of direct materials should have been used. But, 30,000 pounds were used. If there is no price variance, then the extra 3,000 pounds used cost Nulife an extra $3,000. This cost overrun is an unfavorable usage variance. But also like the spending variances, the variance by itself does not indicate its underlying cause(s). This information needs to be obtained from the people responsible for direct materials usage.

Generally, the production manager is responsible for the direct materials usage variance because he or she is in charge of how direct materials are used. In instances where direct materials are substandard, the responsibility may lie with the purchasing department. Other causes include the following:

• Incorrect machine settings or lack of proper tools

• Failure to keep machines and tools in good working condition

• Inexperienced or inefficient workers

• Fatigue caused by pressure to complete a rush order

• Changes in production or quality control methods

• Inadequate blueprints or errors in specifications

• Variations in yield from materials

• Failure to return excess materials to the storeroom

In the Tigerade example, the variance was due to inexperienced workers and improper supervision at mixing vat 3. A total of 3,000 pounds of compound was spilled on the floor and wasted.

The direct materials standard quantity is affected by the desired size, shape, and quality of the finished product, as well as by the kind and quality of the direct materials used to make the product. An allowance for normal spoilage is included in determining practical standard quantities. The tighter the standard, the smaller the allowance for scrap. When appropriate direct materials standard quantities are in effect, control over material losses, waste, and scrap is facilitated, because any usage variance from what was determined to be a reasonable amount can be traced to its source, as was done in the Tigerade example.

Given the kind and quality of direct materials, physical quantity estimates are made in terms of weight, size, volume, or other measure. The standard quantities and quality of direct materials needed to make the product are compiled in its bill of materials within an MRP or MRP II program. The actual quantities are input via bar code scanning devices, or materials requisitions in nonautomated SCASs.

DIRECT LABOR EFFICIENCY VARIANCE. The direct labor efficiency variance measures the productivity of direct labor. The basic formula used to compute this variance is the same as that used for the direct materials usage variance:

Direct labor efficiency variance = SP x (SQA - AQu)

During July, the direct labor efficiency variance for Tigerade was:

Direct labor efficiency variance = $10/DLhr x (18,000 DLhr - 17,500 DLhr)

= $5,000 favorable

Explaining this variance to shop floor personnel, 500 direct labor hours less than expected (the SQA) were worked. At a budgeted labor rate of $10 per DLhr, this resulted in a cost savings of $5,000 (a favorable usage variance). The Tigerade production manager explained that this efficiency was due to the high spirit of the temporary workers. But remember the cause of the direct materials usage variance--by working so fast, they also wasted 3,000 pounds of Tigerade mix.

This observation provides the management accountant with insights into some of the characteristics required in a high-quality SCAS:

For operational control, it is important that the SCAS captures input data about the sources and causes of cost variances. By having shop floor personnel input these data as operations take place, their attention is focused on the need to identify production problems and control them at the source.

In assigning responsibility for cost variances, these source and cause data are critical. To ensure proper performance evaluation and the rewards necessary for proper employee motivation, the SCAS needs to report the sources and causes of cost variances and whether corrective actions have been taken.

As the Tigerade example shows, one decision (activity) may result in more than one cost variance. In other words, cost variances can be related; they are not necessarily financial measures of independent problems. For July production of Tigerade, the hiring of temporary workers resulted in three cost variances: an unfavorable direct materials usage variance of $3,000; a favorable direct labor rate variance of $8,750; and a favorable direct labor efficiency variance of $5,000.

The direct labor efficiency variance is vital for management's review, because increasing productivity in labor-intensive processes is a key to reducing production costs. Generally, this variance is the responsibility of supervisors and workers. In some instances, however, an unfavorable direct labor efficiency variance may stem from areas not controlled by them, such as the following:

• Faulty equipment or materials

• Machine breakdowns

• Lack of materials

• Changes in production processes

Factors that cause the variance to occur can be identified by careful analysis of the operations, which must include discussion with individuals involved in specific areas of the organization. Two important factors used to determine the direct labor standard quantities are:

• Specific operations to be performed

• Amount of labor time to be spent on each operation

Both factors are measured by engineering, production, and management accounting personnel.

Each operation performed by either employees or equipment should be determined. Examples of labor operations are bending, lifting, turning, reaching, moving materials, setting up for a new production run, cleaning up, and reworking. All of these operations will affect the time needed to produce a product. Thus, such operations should be evaluated to determine which are adding value and which can be eliminated or reduced.

Some organizations conduct time and motion studies. During such studies, unusual times due to abnormal conditions should be eliminated. Some industries have developed predetermined times based on standard time and motion studies. Using these data reduces the cost of developing standards for a specific company in one of those industries. Care must be taken, however, to make sure the operations and labor of the company match the operations and labor on which the data were gathered.

Plant layout, equipment conditions, and the workplace should be analyzed, and an effort should be made to improve these to the best practical level (maybe even close to an ideal level). In conjunction with studying and setting direct materials and direct labor standards, purchasing and expediting materials should be studied so that employees have the right materials (quality and quantity) at the right place at the right time. Moreover, employees should be properly trained before being put on the job and should have quick access to complete instructions after being put there.

If direct labor standards are based on a work environment that is conducive to maximum efficient and effective operations, variations of actual from standard become valid indicators of what really should be occurring. A poor workplace that is unsuitable for both people and efficient operations will most likely lead to variances whose underlying causes cannot be easily traced.

The direct labor efficiency variance, however, can encourage costly actions by employees. For example, employees may rush through a process wasting costly materials to improve labor efficiency as happened at Nulife during July.

The direct labor efficiency variance may have little relevance in a highly automated plant that has few employees. For example, some companies, such as Allen-Bradley, manufacture over $100 million worth of products per year and employ only three to five workers.

VARIABLE OVERHEAD EFFICIENCY VARIANCE. The variable overhead efficiency variance is a measure of the excess VOH used solely because the actual direct labor hours worked differed from the standard hours allowed. Tie assumption is that if more direct labor hours are worked, then more VOH items are used (VOH is a variable cost). This variance can be computed using the following formula (the same basic formula used with the direct materials and labor efficiency variances):

VOH efficiency variance = SP x (SQA - AQu)

During July, the VOH efficiency variance for Tigerade production was:

VOH efficiency variance = $1.501DLhr x (18,000 DLhr - 17,500 DLhr)

= $750 favorable

The assumption that more labor usage means more VOH items are used is questionable. For example, the temporary workers at Nulife in July wasted 3,000 pounds of Tigerade mix by working too fast. Did they also use excess VOH items such as supplies? The VOH efficiency variance does not really answer this question, but from looking at the VOH spending variance, it appears that excess usage of indirect items was not a problem. Again, this highlights the major disadvantage of traditional cost variance analysis. Variances alone do not provide information about their real underlying causes.

Whether favorable or unfavorable, the responsibility for this variance lies with the manager in charge of labor for the period (if labor causes VOH usage). Other bases, such as machine hours, can also be used to budget VOH and measure its variances.

Fixed Overhead Cost Variances

LEARNING OBJECTIVE 4

Calculate and interpret the fixed overhead variances.

With each of the variable cost elements, there are fundamentally only two kinds of cost variances, spending and usage. This is also true for fixed overhead, but the formulas for the FOH cost variances differ from the variable cost variances because this cost element behaves differently. It is a fixed cost, not a variable cost.

FIXED OVERHEAD BUDGET VARIANCE. The fixed overhead budget variance is the difference between budgeted fixed overhead costs and actual fixed overhead costs:

Fixed overhead budget variance = Budgeted FOH - Actual FOH

In the Nulife Tigerade example, the following FOH budget variance resulted in July:

Fixed overhead budget variance = $12,000 - $12,100 = <$100> unfavorable

During July, $100 more was spent on FOH items than was budgeted ($12,000 from its manufacturing cost equation in Exhibit 8-2). The unfavorable FOH spending (budget) variance is the responsibility of the various people who have control over the different items that comprise the total budgeted FOH costs. Generally, managers have only limited ability to control FOH costs in the short run, however. Fixed overhead costs are incurred to provide production capacity. In other words, FOH exists because of the production process (the factory) and its size. The bigger the factory, the larger its fixed costs (usually), such as building depreciation, insurance, property taxes, and the costs of heating and air conditioning. Because different people are responsible for different components of FOH, the SCAS should report this variance on a line-item basis, similar to the reporting of the VOH spending variance (see Exhibit 8-3). Exhibit 8-4

|

Exhibit 8-4 Detailed Analysis of the Fixed Overhead Spending (Budget) Variance for Nulife Corporation |

|||

|

Detailed Comparison of Budgeted Fixed Overhead Costs with Actual Fixed Overhead Costs For the Month Ended July 31 |

|||

|

Fixed Overhead Elements |

Budget for July |

Less: Actual FOH Costs |

FOH Budget Variance |

|

Supervisor salaries |

$ 6,000 |

$ 6,500 |

<$500> U |

|

Depreciation |

4,000 |

4,000 |

-0- |

|

Insurance |

1,500 |

1,000 |

500 F |

|

Property taxes |

500 |

600 |

< 100> U |

|

Totals |

$12,000 |

$12,100 |

<$100> U |

|

Explanation of variances: Supervisor salaries variance of $500 U is due to a raise in pay. Insurance variance of $500 F is caused by an unexpected reduction in premium due to an improvement in the employee safety program. Property taxes variance of $100 U is caused by a new taxing formula passed by the city council this month. |

|||

illustrates a line-by-line FOH budget variance report.

Any control that is to be exerted over FOH must take place when managers are preparing the annual budget, modifying it during the year, and/ or planning capacity changes. Fixed overhead items, therefore, are usually not subject to as much day-to-day, or even month-to-month, control as are variable cost items.

FIXED OVERHEAD PRODUCTION VOLUME VARIANCE. This variance is usually called the fixed overhead volume variance, or just the volume variance. It is a usage variance in that it measures how well the factory as a whole was used. Since the costs of the factory are FOH costs, this is an FOH usage variance. It can be calculated by either of two formulas:3

FOH volume variance

= FOH standard cost x (Actual output - Production quota)

or:

= FOH standard price x (SQA - Budgeted DLhr)

The second formula more closely resembles the formula for variable cost usage variances and may be easier to learn because of its similarity to the other usage variance formulas. First, the basis for applying FOH has to be known. This information is in the standard cost card (Exhibit 8-2 for Tigerade). Fixed overhead is applied to cases of Tigerade based on the DLhr worked. Thus, the standard hours allowed (SQA) and the budgeted DLhr need to be calculated in order to use this version of the volume variance formula. The budgeted DLhr for July were 20, 000.4 Using DLhr and the FOH POR in this formula:

FOH volume variance = $0.60/DLhr x (18,000 DLhr - 20,000 DLhr)

= <$1,200> unfavorable

If the FOH POR (standard price for FOH) is based on machine hours, then the standard machine hours allowed and the budgeted machine hours would be used.

The first version of this variance formula may be easier to explain, however. To illustrate, the FOH volume variance for Tigerade is calculated as:

FOH volume variance = $1.20/case x (9,000 cases - 10,000 cases)

= <$1,200> unfavorable

The FOH volume variance measures how efficiently the entire plant is used. Using the output-based formula, 10,000 cases of Tigerade were budgeted for July production. The FOH cost budgeted was $12,000 (reference the cost equation in Exhibit 8-2). Thus, only $1.20 of FOH cost had to be absorbed by each case (this is the FOH standard cost). In other words, if the sales price is increased by $1.20 per case, and 10,000 cases are produced and sold, Nulife will receive extra sales revenues of $12,000 that can be used to pay for the FOH. One of the benefits of a standard absorptive manufacturing cost is that it serves as an aid to adequate sales price setting.5

In July, however, Nulife produced only 9,000 cases of Tigerade, not the 10,000 planned for. Thus, there were 1,000 cases not produced and not sold. Because these cases were not sold, Nulife cannot recover the extra $1.20 from each needed to pay for the FOH costs. The 1,000 cases not produced, multiplied by the $1.20 FOH standard cost, equals $1,200 (10 percent of the $12,000 budgeted FOH). This $1,200 of sales revenues is needed to pay for the last $1,200 of FOH costs. Since the revenues are not there, the remainder of the FOH will have to he paid for out of the profits made on the 9,000 cases produced and sold. Total profits will be $1,200 less than they should have been for the 9,000 cases sold, because the production quota was not met. Because the plant was not used as efficiently as planned, profits went down. This is equivalent to the lower profits that result from inefficient use of labor or materials (their usage variances). The plant is just another manufacturing resource, like materials and labor, and using it inefficiently creates a usage variance just like the other manufacturing inputs.

The usefulness and interpretation of the FOH volume variance depend on the volume used in calculating the FOH standard cost. In the Nulife situation, expected capacity was used. Nulife could have used normal, practical, or theoretical capacity (refer back to Exhibit 7-9). If any of these three options had been chosen, the usefulness and interpretation of the FOH volume variance would have been different.

For example, WCM proponents might use theoretical capacity in determining the FOH standard cost. The difference between this maximum productive capacity and the actual output measures how much of the plant is idle. While this may be by design, a continuous improvement philosophy means that the volume variance should get smaller over the years. Here is yet another example of how a high-quality SCAS should report long-run trends in variances.

When expected capacity is used to set the FOH standard cost, an unfavorable volume variance is due to lower than budgeted production. This is often caused by a lack of sales orders. Lack of sales orders may be caused by one or a combination of the following:

• High prices for the product

• Low quality of the product

• Inadequate advertising and lack of aggressive sales campaigns

• Inability to deliver when customers want the product

• Economic recession

Some other causes of unfavorable volume variances are controllable by plant management:

• Poor job scheduling

• Excessive employee absenteeism

• Shortage of direct materials and supplies due to poor planning

• Breakdown of machines due to poor preventive maintenance

• Inadequate training or supervision of workers

COMBINING THE OVERHEAD VARIANCES. In the preceding discussions, two variances (spending and usage) were calculated for each cost element (direct materials, direct labor, VOH, and FOH). Note that for overhead, spending and usage variances were separately calculated for VOH and FOH, resulting in a total of four overhead cost variances. These were separately calculated because the variances are controlled by different people (responsibility centers).

In traditional CAS designs, though, VOH and FOH were not separately accounted for. In Chapters 4, 5, and 6, VOH and FOH were combined into just one total overhead (TOH) account, and only one TOH POR was used to apply overhead to products. Unless VOH and FOH are separated in the SCAS, calculating four overhead variances is difficult.

Consequently, in many traditional SCASs, fewer than four overhead variances were prepared for management. Presenting all four overhead variances is called “four-way analysis of overhead.” Sometimes only three overhead variances are calculated (“three-way” analysis), or only two variances (“two-way” analysis), or just one TOH cost variance (“one-way” analysis).

These simpler presentations result in less useful information and degrade the quality of the SCAS. Nevertheless, these methods still often appear on professional accounting certification exams (CPA, CMA, CIA), so they will be briefly illustrated here. There are two “tricks” to remember in performing three-way, two-way, or one-way overhead analysis. First, four overhead variances have already been calculated. In three-way analysis, two variances are added together. In two-way analysis, three of the four overhead variances are added together. In one-way analysis, all four overhead variances are added together.

The second “trick” is to know which variances to calculate first. This involves two steps. The first variance to calculate is the total overhead variance. This is the sum of the four variances and represents the one-way method. The total overhead variance is the difference between the TOH applied to production and the TOH actually incurred:6

For Tigerade,

TOH applied = TOH POR x SQA

TOH applied = $2.10/DLhr x 18,000 DLhr = $37,800

The actual TOH in July equalled $37,100 (VOH of $25,000 plus FOH of $12,100 as shown in Exhibit 8-2). The difference is $700 favorable. This can be verified by adding together the four overhead cost variances:

VOH spending variance = $1,250 favorable

VOH efficiency variance = $750 favorable

FOH budget variance = < 100> unfavorable

FOH volume variance = <1,200> unfavorable

TOH variance = $ 700 favorable

The second variance to calculate is the FOH volume variance. This variance is one of the cost variances in two-way, three-way, and four-way analysis. Knowing the TOH variance and the FOH volume variance, two- and three-way analysis can be quickly performed.

In two-way analysis, the two variances are the FOH volume variance and the “everything else” variance. This is simply the difference between the TOH variance and the FOR volume variance and is often labelled the “TOH budget variance”:

TOH variance = $ 700 favorable

Less FOH volume variance = < 1,200> unfavorable

TOH budget variance = $1,900 favorable

This is also the sum of “everything else” (VOH spending and efficiency, and FOH budget variances).

To prepare three-way analysis, calculate the VOH efficiency variance. The three cost variances arc the FOH volume variance, the VOH efficiency variance, and “everything else” (the sum of the VOH spending and FOH budget variances, which is often called the TOH spending variance).

Summary Of Cost Variance Formulas

Cost variance analysis is really not as difficult as it may seem at this moment. There are only two types of cost variances, spending and usage. There are four kinds of manufacturing inputs: direct materials, direct labor, variable overhead, and fixed overhead. Since each has its own spending and usage variance, there are eight cost variances in total. All of the variable costs, though, use the same formula for their spending variances. They also use the same formula for their usage variances. The fixed overhead variances' formulas are a little different. The formulas are summarized in Exhibit 8-5.

|

Exhibit 8-5 Cost Variance Formulas |

||

|

COST VARIANCE ANALYSISa |

||

|

Types of Cost Variances |

Spending |

Usage |

|

Inputs: |

AQp (SP - AP)b |

SP (SQAc - AQu) |

|

Direct materials Direct labor Variable overheadd |

||

|

Fixed overhead (Spending = “Budget” usage = “Volume”) |

Budgeted FOH -AC |

SPFOH (SQA - Budgeted DLhr) or SCFOH (Actual output - Budgeted output) |

|

|

||

|

a Note: Whether four-way, three-way, or two-way, the TOH cost variance = =Applied TOH - ACOH =(SPTOH x SQA)-ACTOH In four-way: TOH cost variance = VOH spending + FOH budget + VOH usage + FOH volume In three-way: TOH cost variance = TOH spending + VOH usage + FOH volume In two-way: TOH cost variance = TOH budget + FOH volume (Hint: In two-way and three-way, always calculate TOH cost variance and FOH volume.) bAP can be calculated if not known: AP x AQ = AC. Thus, AP = AC + AQ. cSQA = SO x Actual output. dThis is four-way overhead cost variance analysis (2 VOH cost variances + 2170H cost variances) |

The cost variances also can be combined into. a general model approach to cost variance analysis. This is accomplished by grouping the direct materials variances together, then the direct labor, VOH, and FOB variances. The general model also includes the total cost variance for each input. Exhibit 8-6 presents this general model approach for Nulife's Tigerade variances for direct materials and direct labor during July.

|

Exhibit 8-6 Analysis of Direct Materials and Direct Labour Variances for Nulife Corporation |

||||

|

|

Direct Materials Variances |

|

||

|

1 |

|

2 |

|

3 |

|

Actual direct materials costs Actual quantity purchased x Actual price |

|

Actual inputs at standard prices Actual quantity x Standard price |

|

Outputs at standard costs Standard quantity allowed x Standard price |

|

40,000 lbs. x $1.10 = $44;000 |

40,000 lbs. x $1.00 = $40,000 |

|

30,000 lbs. x $1.00 = $30,000 |

27,000 lbs. x $1.00 = $27,000 |

|

40,000 lbs. x $0.10 = $4,000 Purchase price variance $4,000 U |

|

3,000 lbs. x $1.00 = $3,000 Usage variance $3,000 U

|

||

|

|

Total direct materials variance $7,000 U |

|

||

|

|

|

|

|

|

|

|

Direct Labor Variances |

|

||

|

Actual direct labor costs Actual DLhr x Actual rate |

|

Actual inputs at standard rates Actual DLhr x Standard rate |

|

Outputs at standard costs Standard DLhr allowed x Standard rate |

|

17,500 DLhr x $9.50 = $166,250 |

|

17,500 DLhr x $10.00 = $175,000 |

|

18,000 DLhr x $10.00 = $180,000 |

|

|

|

|

|

|

|

|

17,500 DLhr x $0.50 = $8,750 Rate variance $8,750 F |

|

500 DLhr x $10.00 = $5,000 Efficiency variance $5,000 F |

|

|

|

|

Total direct labor variance $13,750 F |

|

|

Exhibit 8-7 illustrates the variable and fixed overhead cost variances for Tigerade.

|

|

|

Variable Overhead Variances |

|

|

|

Actual variable overhead costs |

|

Actual inputs at standard prices |

|

Outputs at standard cost |

|

$25,000 |

|

Actual DLhr x VOH POR 17,500 DLHr x $1.50 = $26,250 |

|

Standard DLhr allowed x VOH POR 18,000 DLHr x $1.50 = $27,000 |

|

|

|

|

|

|

|

|

$25,000 - $26,250 |

|

500 DLhr x $1.50 = $750 |

|

|

|

Spending variance $1,250 F |

|

Efficiency variance $750 F |

|

|

|

|

Total variable overhead variance $2,000 F |

|

|

|

|

|

|

|

|

|

|

|

Fixed Overhead Variances |

|

|

|

Actual fixed overhead costs |

|

Budgeted fixed overhead costs |

|

Outputs at standard cost |

|

|

|

Budgeted DLhr x FOH POR |

|

Standard DLhr allowed x FOH POR |

|

$12,100 |

|

20,000 DLhr x $0.60 = $12,000 |

|

18,000 DLhr x $0.60 = $10,800 |

|

|

$12,100 - $12,000 |

|

2,000 DLhr x $0.60 = $1,200 |

|

|

|

Spending (budget) variance $100 U |

|

Production volume variance $1,200 U |

|

|

|

|

Total fixed overhead variance $1,300 U |

|

|

|

|

|

|

|

|

Scas Journal Entries

LEARNING OBJECTIVE 5

.Prepare the journal entries for an SCAS, and the cost variance report.

SCASs can be used in job order, process, and JIT systems. Jobs, departments, or cells (in a JIT) are debited with the costs of the manufacturing inputs used. The journal entries in an SCAS, versus a normal JOCAS or PCAS, differ in two basic ways, however:

First, in an SCAS, the cost amounts used are not the same as in a PCAS or JOCAS. Instead of recording actual costs, all cost elements are recorded at standard cost allowed (SCA). SCA is the standard cost for each input multiplied, by production volume. To demonstrate, the standard cost for direct materials in Tigerade (Exhibit 8-2) is $3 per case. If 10 cases are produced, the SCA is $30 for direct materials, and this is all that will be charged to its cost for direct materials. For production of 10 cases, the direct labor SCA is $200. The VOH and FOH SCAs for 10 cases are $30 and $12, respectively. Either of two formulas can be used to calculate SCA:7

SCA = Standard cost x Actual output

= Standard price x Standard quantity allowed (SQA)

In an SCAS, the total production cost assigned to 10 cases of Tigerade is $272. This is calculated by simply summing the SCA for each input item or by the following formula:

Total production cost = SAMC x Actual production volume

= $27.20/ case x 10 cases

= $272.00

The second difference between normal and SCAS journal entries is related to the first. Since all inputs, and production volume in total, are costed at standard, then the difference between SCA and actual cost also is journalized.

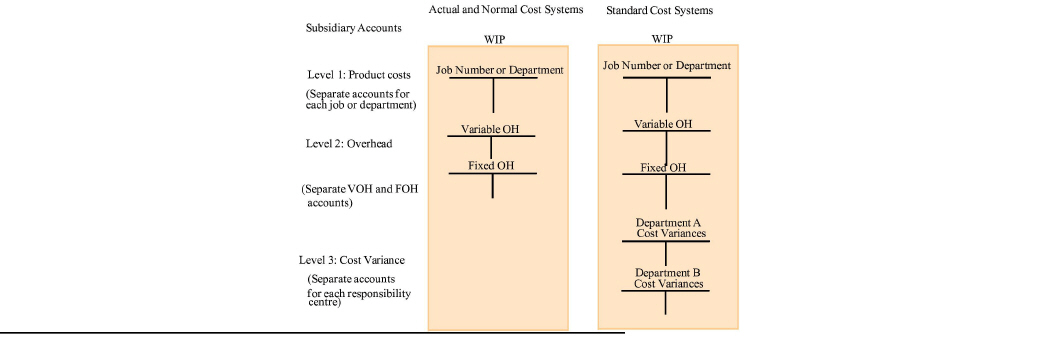

In other words, each cost variance is journalized into its own subsidiary y account. Actual and normal cost systems have two “levels” of general ledger subsidiary accounts, product costs and overhead. SCASs have three “levels” of subsidiary accounts. This is highlighted in Exhibit 8-8

|

.

In Exhibit 8-8separate VOH and FOH subsidiary WIP accounts are created, consistent with the discussion of separately budgeting for each of these cost elements in Chapter 7. Chapter 7 also pointed out the need to assign cost variances to responsibility centers for proper performance evaluation. This is illustrated in Exhibit 8-8 by having two production departments (A and B), each with its own subsidiary cost variance account. This exhibit should be compared to Exhibits 4-2 (basic CAS), 5-1 (JOCAS), and 6-4 (PCAS).

Standard Pcas Journal Entries

In Chapter 4, three basic types of journal entries were identified:

• Purchasing inputs (materials, labor, and overhead)

• Using inputs in manufacturing (materials requisitions, labor distribution, and overhead applications)

• Transferring completed production (between departments in a PCAS, to FGI for COGM, and to COGS when sold)

PURCHASING MANUFACTURING INPUTS. Journal entry 1 records the purchase of raw materials. In the SCAS for Nulife (Exhibit 8-2), the journal entry to record the purchase of Tigerade drink mix (its direct material) is:

|

JOURNAL ENTRY 1: Direct Materials Purchases |

||

|

RMI-Tigerade Mix (SP x AQp = $1.00/lb. x 40,000 lb.)RMI-Tigerade Mix |

$40,000 |

|

|

Price Variance [AQp x (SP - AP) = 40,000 lb. X($1.00/lb. - $1.10/lb.)] |

$ 4,000 |

|

|

Accounts Payable (AP x AQp = $1.10/lb. x 40,000 lb.) |

|

$44,000 |

Tigerade mix, being a special direct material, has its own subsidiary ledger account within RMI. The price variance is recorded when the materials that create it are received.

An unfavorable cost variance is debited to the cost variance account. An unfavorable cost variance is a cost overrun. Paying for this increased cost reduces (credits) cash. If cash is credited, then the cost variance account must be debited. Conversely, a favorable cost variance is a credit amount within the journal entries. Favorable variances are cost savings. Saving costs increases (debits) cash. Thus, the cost variance account is credited.

The information explaining the variance should be available from the purchase order for entry into the SCAS. If a record field is established for the explanation, or a general ledger coding system is created to identify its cause, then the cause can be input and reported. The ability to capture and report information on the causes of cost variances is a characteristic of a high-quality SCAS.

Journal entries 2 and 3 recording payroll and the employer's related liabilities are the same in all CASs. In recording actual overhead costs (journal entry 4), separate WIP subsidiary accounts are created for VOH and FOH. Assume that the $25,000 in actual VOH costs (Exhibit 8-2) represents utilities costs for July that are paid for in cash and that the $12,100 of FOH represents July's factory depreciation. Journal entry 4 to record these costs is:

|

JOURNAL ENTRY 4: Other Overhead Costs Incurred |

||

|

WIP-VOH (Utilities) |

$25,000 |

|

|

WIP--FOH (Depreciation) |

$12,100 |

|

|

Cash |

|

$25,000 |

|

Accumulated Depreciation |

|

$12,100 |

USING MANUFACTURING INPUTS IN PRODUCTION. Journal entries 5-7

record the issuance of materials, labor, and the application of overhead to production departments. When the journal entries for assigning these costs were made in a normal PCAS, each department was charged with the materials and labor costs directly traced to it and with the overhead applied to it. This resulted in multiple subsidiary accounts (one for each department) being debited in journal entries 5-7.

In a process costing SCAS, though, each department's usage is journalized separately. To illustrate, instead of having one journal entry 5 for direct materials used in Departments A and B, a separate journal entry is made just for Department A's usage. Another journal entry is made to record direct materials usage in Department B. Preparing individual journal entries for each department's usage of direct materials, direct labor, and applied overhead facilitates the recording and control of each department's cost variances. To demonstrate using the Tigerade example, assume that the costs shown in Exhibit 8-2 are only for Department A:

|

JOURNAL ENTRY 5: Direct Materials Requisitions |

||

|

WIP-Department A (DM)(SP x SQA = $1.00/lb. x 27,000 lb.) |

$27,000 |

|

|

WIP-Department A DM Usage Variance [SP x (SQA - AQu) = $1.00/lb. x (27,000 lb. - 30,000 lb.)] |

$ 3,000 |

|

|

RMI - Tigerade Mix (SP x AQu = $1.00/lb. x 30,000 lb.) |

|

$30,000 |

Because the price variance was already recorded in journal entry 1 when the direct materials were purchased, materials enter RMI at their standard price. Thus, when these materials are requisitioned into the production department, they are taken out of (credited to) RMI at standard price.

Notice that the usage of direct labor and overhead are recorded by a different method. These were journalized (debited) into their “temporary holding accounts” at their actual costs. When these inputs are used in production, they arc removed (credited) from their holding accounts at actual cost. The SCA is debited to WIP (as was done above for direct materials), and both the spending and usage variances are recorded in journal entries 6 and 7:

|

JOURNAL ENTRY 6: Direct Labor Distribution |

||

|

WIP-Department A (DL)(SP x SQA = $10.00/DLhr x 18,000 DLhr) |

$180,000 |

|

|

WIP-Department A DL Rate Variance [AQ x (SP - AP) = 17,500 DLhr X($10.00/DLhr - $9.50/DLhr)] |

|

$ 8,750 |

|

WIP-Department A DL Efficiency Variance [SP x (SQA - AQ) = $10.00 DLhr X(18,000 DLhr - 17,500 DLhr)] |

|

$ 5,000 |

|

Gross Wages (Actual cost = AP x AQ = $9.50/DLhr X17,500 DLhr) |

|

$166,250 |

|

|

|

|

|

JOURNAL ENTRY 7a: VOH Applied |

||

|

WIP-Department A (VOH Applied) SP x SQA = $1.50/DLhr x 18,000 DLhr) |

$27,000 |

|

|

WIP-Department A VOH Spending Variance [(AQ x SP) - AC = (17,500 DLhr x $1.50/DLhr) - $25,000] |

|

$ 1,250 |

|

WIP-Department A VOH Efficiency Variance [SP x (SQA - AQ) = $1.50/DLhr X(18,000 DLhr - 17,500 DLhr)] |

|

$ 750 |

|

WIP-VOH (Actual cost) |

|

$25,000 |

|

JOURNAL ENTRY 7b: FOH Applied |

||

|

WIP-Department A (FOH Applied) (SP x SQA = $0.60/DLhr x 18,000 DLhr) |

$10,800 |

|

|

WIP-Dept. A FOH Budget Var (Budgeted FOH - Actual FOH = $12,000 -$12,100) WIP-Dept. A FOH Volume Var [SP x (SQA - Budgeted DLhr) = $0.60/DLhr x (18,000 DLhr - 20,000 DLhr)] WIP-FOH (Actual cost) |

$ 100

$ 1,200 |

$12,100 |

In the above journal entries, each Department A cost variance has its own subsidiary account. When this is compared to Exhibit 8-8, it is clear that the Exhibit 8-8 cost variance accounts for Departments A and B are actually control accounts. The reason for having individual subsidiary accounts for each department's cost variances is that some of the variances may not be the responsibility of the department's manager. By having separate variance accounts in the general ledger system, the account balances can be reported to the responsibility center that really caused each variance.

JOURNAL ENTRIES FOR COMPLETED PRODUCTION. The production costs have been debited to the department's subsidiary ledger account at SCA. Thus, when output is transferred to the next department or to FGI, and then to COGS, SCA is the amount to use in journal entries 8-10:8

|

JOURNAL ENTRY 8: Transferring Output to Department B |

||

|

WIP-Department B(SAMC x Actual output = $27.20/case x 9,000 cases) |

$244,800 |

|

|

WIP-Department A |

|

$244,800 |

To demonstrate the transfer of finished goods from the factory to finished goods inventory, assume that Tigerade is moved from Department A to FGI:

|

JOURNAL ENTRY 9: Cost of Goods Manufactured |

||

|

FGI-Tigerade |

$244,800 |

|

|

WIP-Department A |

|

$244,800 |

Finally, the journal entry to record COGS is:

|

JOURNAL ENTRY 10: Cost of Goods Sold |

||

|

COGS-Tigerade |

$244,800 |

|

|

FGI-Tigerade |

|

$244,800 |

Standard Jocas Journal Entries

Traditionally, SCASs have been used more in PCASs than in JOCASs. However, the need for effective and efficient cost management is just as crucial in job order systems as it is in process systems. This was first demonstrated in Chapter 5 in the illustration of construction cost budgeting and control (Exhibits 5-21 and 5-22).

In job order enterprises (e.g., construction, print shops), in for-profit services (CPAs, engineers, and lawyers), and in certain merchandising firms (such as distribution centers), the need for cost control is fast becoming a serious management concern. This is also true in nonprofit services, such as hospitals and government services. With increasing public and national concern over health care cost management, the role of the modern management accountant is becoming more important. Standard costing and cost variance analysis can have a significant impact on cost management in the economy's service sector.

Whether cost variances are journalized within the SCAS or just calculated and reported within a normal JOCAS, information about them is essential for proper cost management. One advantage of journalizing cost variances is that the subsidiary accounts provide the basis for reporting this information. The cost variances are isolated within separate accounts, and a formal record exists within the SCAS for both short-run cost variance reports and long-run trend analyses.

In designing the general ledger system for WIP, level 1 subsidiary accounts are established by department in a PCAS and by job in a JOCAS. This only creates a difference in journal entries 5-7 representing the use of manufacturing cost elements in production. Continuing the Tigerade example, assume the 9,000 cases produced in July was just one job order (482) and that there are still two production departments. As with the PCAS journal entries above, the costs incurred in Exhibit 8-2 are for Department A. In a standard JOCAS, these journal entries become:

|

JOURNAL ENTRY 5: Direct Materials Requisitions |

||

|

WIP-Job 482 (Department A DM)(SP x SQA = $1.00/lb. x 27,000 lb.) |

$27,000 |

|

|

WIP-Dept. A DM Usage Variance (Job 482)[SP x (SQA - AQu) = $1.00/lb. x (27,000 lb. - 30,000 lb.)] |

$ 3,000 |

|

|

RMI-Tigerade Mix (SP x AQu = $1.00/lb. x 30,000 lb.) |

|

$30,000 |

|

JOURNAL ENTRY 6: Direct Labor Distribution |

||

|

WIP-Job 482 (Department A DL)(SP x SQA = $10.00/DLhr x 18,000 DLhr) |

$180,000 |

|

|

WIP-Dept. A DL Rate Variance (Job 482) [AQ x (SP - AP) = 17,500 DLhr x ($10.00/DLhr - $9.50/DLhr)] |

|

$ 8,750 |

|

WIP-Dept. A DL Efficiency Variance (Job 482) [SP x (SQA - AQ) = $10.00/DLhr x (18,000 DLhr - 17,500 DLhr)] |

|

$ 5,000 |

|

Gross Wages (Actual cost = AP x AQ = $9.50/DLhr x 17 500 DLhr) |

|

$166,250 |

|

JOURNAL ENTRY 7a: VOH Applied |

||

|

WIP-Job 482 (VOH Applied) (SP x SQA = $1.50/DLhr x 18,000 DLhr) |

$27,000 |

|

|

WIP-Dept. A VOH Spending Variance (Job 482) [(AQ x SP) - AC =(17,500 DLhr x $1.50/DLhr) - $25,000] |

|

$ 1,250 |

|

WIP-Dept. A VOH Efficiency Variance |

|

$ 750 |

|

(Job 482) |

|

|

|

[SP x (SQA - AQ) = $1.50/DLhr X(18,000 DLhr - 17,500 DLhr)] |

|

|

|

WIP-VOH |

|

$25,000 |

|

(Actual cost) |

|

|

|

JOURNAL ENTRY 7b: FOH Applied |

||

|

WIP-Job 482 (FOH Applied) (SP x SQA = $0.60/DLhr x 18,000 DLhr) |

$10,800 |

|

|

WIP-Dept. A FOH Budget Variance (Job 482) (Budgeted FOH - Actual FOH = $12,000 -$12,100) |

$ 100 |

|

|

WIP-Dept. A FOH Volume Variance (Job 482) [SP x (SQA - Budgeted DLhr) = $0.60/DLhr X(18,000 DLhr - 20,000 DLhr)] |

$ 1,200 |

|

|

WIP-FOH (Actual cost) |

|

$12,100 |

|

|

|

|

The amounts calculated are the same as in a standard PCAS. There are only two differences in the general ledger account titles;

• The WIP subsidiary accounts for product costs are organized by jobs instead of by departments.

• The department cost variance accounts have posting references for cost variances caused within specific jobs.